Active vs. Passive Investing

[rewrite as whether to use a collection of ETFs, a collection of stocks, or both, and extend]

Everyone has different strategies for approaching investing. Some want hands-on quantitative-based investing that they can know the ins and outs of. Others are more willing to invest and let their money grow without worrying about it. This article will discuss the difference between both methods, the time investment, key terms, and which is more likely to perform positively.

What is Active and Passive Investing?

To determine which of these methods fits our investing needs, we must first understand exactly what they are. Passive investing assumes that the general market is efficient and that picking your own companies is pointless. Investments typically come in the form of index funds. Active investing is taking control of your investment portfolio and selecting companies yourself. Since the recession, passive investing has consistently been the better performer of the two.

Time requirements of both

A significant difference, beyond performance, is the time commitment required to successfully run a portfolio. Which of these two methods requires more time?

Of the two, active management does require more time. This depends entirely on the active management type. However, we can assume you’ll spend more time under this management style. A couple of examples of active management are as follows;

- Constantly analyzing and buying/selling positions in your portfolio.

- Adding companies to your portfolio without the intention of ever selling them.

- One massive concentrated position that you sell long-term calls against.

- Even if you have a 10-year outlook on the stocks you buy, you are still active in the investment process.

Some of these strategies are more strenuous than others. However, they all actively manage a portfolio of stocks – even if you buy companies and walk away.

On the other hand, passive investing requires minimal effort. Beyond selecting the index fund(s) initially, you will have exposure to a pool of potentially thousands of companies. You don’t need to constantly check each company’s health and rely more on the power of diversification.

Suppose you have multiple funds in your portfolio. In that case, you may want to rebalance how much of each fund you hold at the end of each year in order to keep the weights fairly consistent. Beyond that, passive investing requires you to sit back and enjoy any returns on the index, which doesn’t require much time.

What is an Index Fund?

Index funds are typically structured like mutual funds. They require oversight from a team, and the underlying portfolio does need to be managed. As a result, index funds do charge a small fee to hold them on an annual basis. This fee typically ranges from 10-20 basis points for larger funds like $SPY and $IWM. That said, for 10 basis points, can you gain exposure to over 2,000 companies? How often will you hold 2,000+ companies in your personal portfolio outside of an index fund? How much would that cost you?

On top of saving you some money on transaction costs, index funds don’t need to buy/sell positions nearly as often as a traditional mutual fund. This will benefit you as an investor because all capital gains from mutual funds are passed directly to you. By minimizing the number of transactions made, these funds can minimize your tax bill – to some degree.

Efficient Market Hypothesis

A number of people who swear by investing passively are supporters of the efficient market hypothesis, which, at its core, assumes that there is no benefit to trading within the market since all news is already factored into the price of the stock. Within the efficient market hypothesis, there are three main viewpoints –

• Strong form – the price of stocks fully reflect BOTH private and public information.

• Semi-Strong Form – The price of the stock fully reflects all public information

• Weak Form – The stock price doesn’t reflect either, and investments like value investing become possible.

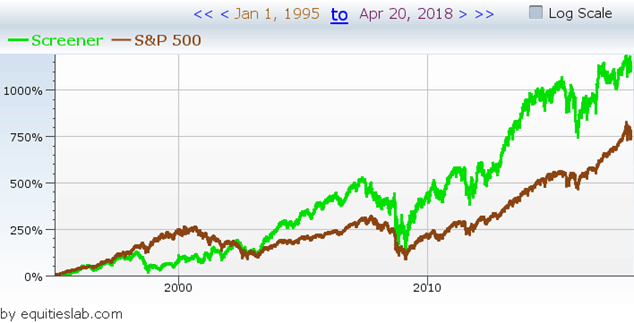

At Equities Lab, we are firm believers in the weak market hypothesis. No matter how rational we’d like to think the markets are, the old saying “The markets can stay irrational longer than you can remain solvent” seems to ring true more often than not. This can easily be proved by running a quick backtest on a value strategy – a style of investing that should not be possible under either the strong or semi-strong form.

This strategy doesn’t skyrocket to the moon over the past 23 years, but it does beat the market, suggesting that there is a bit of merit to the weak form of the efficient market hypothesis.

Why Passive Investing

So there is some merit to the weak form, and it does appear that you could have beaten the market using a fairly simple strategy over the past 23 years, but that required a lot of effort to ensure your portfolio was exactly how you wanted it. On the flip side, the S&P did pretty well over that same period, and all you would have had to do was set it and forget it.

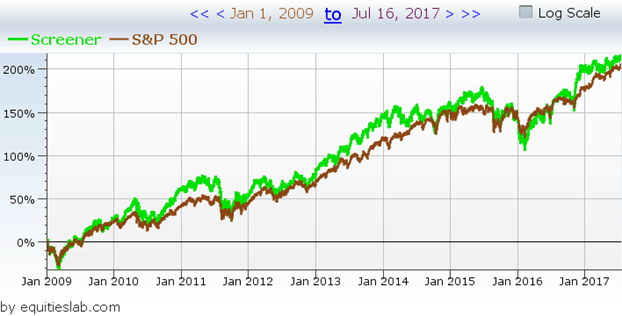

Since the recession, index funds like the $SPY and $IWM have done incredibly well, returning roughly 300% in total since early 2009. You would have had only 1 commission payment with a small annual fee and extreme diversification at your fingertips, and you wouldn’t have had to do anything but buy one fund one time 9 years ago. Not bad for 30 seconds’ worth of work.

Since the recession, index funds like the $SPY and $IWM have done incredibly well returning roughly 300% in total since early 2009. You would have had only 1 commission payment with a small annual fee and extreme diversification at your fingertips, and you wouldn’t have had to do anything but buy one fund one time 9 years ago. Not bad for 30-seconds worth of work.

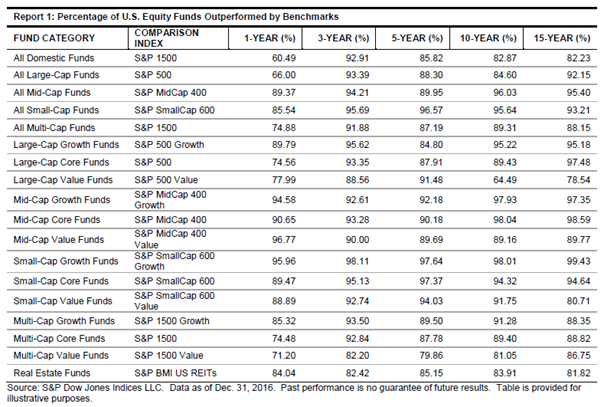

Taking it a step further, how likely do you think it really is to beat the market in the past three, five, or even ten years? The answer is pretty low to be entirely honest. Only about 1-in-10 active managers beat the market in the past ten years. All that work to not beat the benchmark paints a pretty dim picture.

But is it Possible to Outperform?

Of course it’s possible to outperform, we showed that in the value based strategy earlier in the article. However, those returns were a bit sporadic and a couple of years really made all of the difference in the success of that strategy. There are a couple of strategies that do outperform the market fairly consistently and generate alpha for the investor.

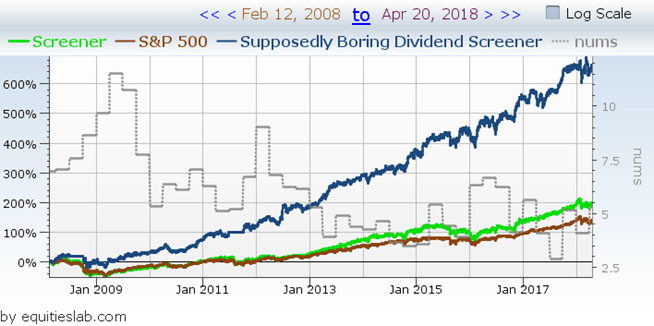

One such strategy is dividend based – a market section that has done incredibly well since the recession. Many large, boring, dividend producing companies were absolutely crushed in the great recession. Since then, they have all worked incredibly hard to claw their way back to where they were originally, while attempting to not change dividend values. The recession is long over with now, but these companies are still strong long term investments.

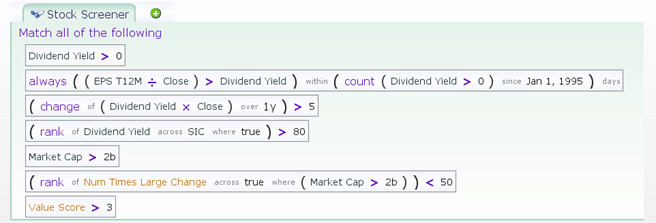

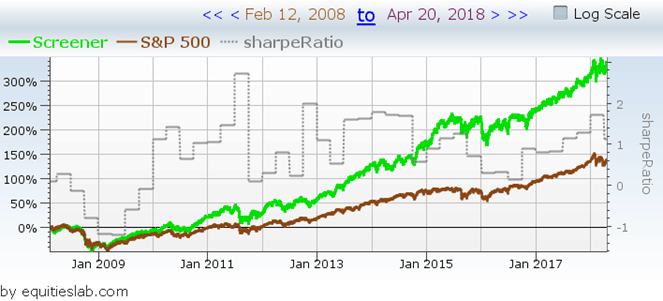

Since 2008, this strategy has returned roughly 600% overall and has beaten the market 9 out of the 10 years it was backtested over.

Here are the parameters of the above backtest. This screen has been featured in its own article, and a link to the Featured Dividend Screener is featured here.

Outperforming with Growth Companies

Dividends don’t really fit in everyone’s portfolio. One alternative is to take a look at growth companies. In this context “growth” isn’t talking about the stock price or the momentum of volume; rather, it references the fact that key earnings components are increasing and the company is generating this growth healthily.

In the Manzitti Profit Quality screen you get slightly smaller returns than the Dividend Screener over the past 10 years, but you do get consistent earnings.

With this strategy you have historically gotten a 15% annual growth rate, a Sharpe ratio of 1.128 annually and a 60% win rate.

Does Active Management win this often?

Though you’ve just been shown two different strategies that have beaten the market over the past ten years, and have actually beaten the market fairly consistently over the past twenty years, the chart indicating the percentage of active managers that outperform the market is fairly small. There are thousands of strategies that do make money, they just don’t generate alpha when compared to the benchmark.

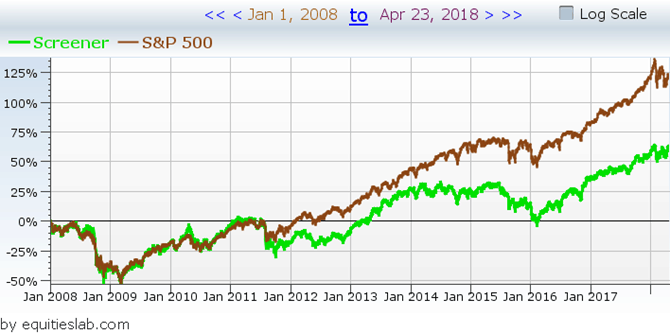

A prime example of this is a favorite screen among the technical analysis community – buying companies that cross below the 200 day moving average. It’s an incredibly simplistic screen that could possibly be refined for better performance, but at this fundamental level, you do make money, just not enough to beat the benchmarked S&P 500.

From all other aspects, this strategy isn’t a bad one. You have a 50% win rate, you get a 5% annualized return, and volatility isn’t too bad. If you work at it you might be able to get it to generate some level of alpha, but then you have to ask yourself how long that will last as all strategies have their ups and downs.

The Decision

The correct decision in the Passive vs. Active debate is that there is no correct decision. Invest how you see fit. There will be times where active management beats passive management, and vice versa. At the end of the day, just know what you’re buying and stick through the tough times. There is always a light at the end of the tunnel.