CAPM – Capital Asset Pricing Model

What does CAPM stand for? Capital Asset Pricing Model.

The CAPM is a staple of nearly every finance course that focuses on the valuation of equity investments. Though it may be an excellent way to begin the process of teaching students how to effectively analyze securities, several assumptions make it very difficult to use in a real-world setting.

In this article, we will talk about the formula, assumptions about the model, an example, and the takeaways.

Formula

E[ri]=rf+Bi(E(rm)-rf)

- E[ri]= Asset return

- Rf= Risk free rate

- Bi= Beta for asset

- E(rm) = Market return

False Assumptions About CAPM

These assumptions are as follows –

- Investors hold a diversified portfolio

- If you have a large enough portfolio or are focused entirely on ETFs, you may be able to get rid of the majority of the unsystematic risk within your portfolio. However, for many people, they are looking to analyze individual companies and project their returns.

- Single-period transaction horizon

- If you are consistently rebalancing your portfolio, this assumption isn’t detrimental to the average portfolio, but if you are holding for longer than a single period, the model falls apart.

- Investors can borrow and lend at a risk-free rate of return

- Investors can easily lend at this rate, but they are unlikely to borrow at this rate as they are not large institutions with access to those sorts of credit lines.

- Perfect capital markets

- If you look at markets as a whole, including all traded financial instruments, you may get an efficient market, but as an equity investor, “the market” typically denotes the S&P 500, which is a much smaller representation of the general market.

We can already see that the CAPM may not be a good tool for investing in individual securities, but without testing, we can’t say that for certain.

Testing Out CAPM

Before we create the CAPM in Equities Lab, we need the general formula to build from.

EquitiesLab CAPM Formula

First, we create the CAPM formula using the most common period of 1 year as our single-period assumptions.

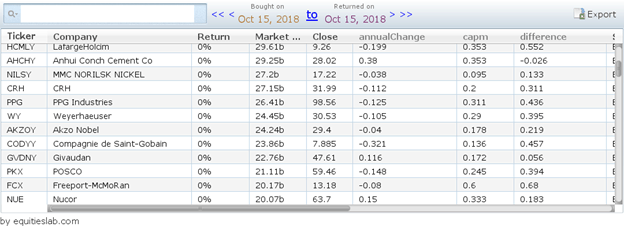

Using the basic screener for Basic Materials within the Equities Lab software, we are presented with 201 matches. Since we don’t have future data, we can see how accurate the CAPM was over the past year when compared with the returns of each company.

These three tabs only plot the CAPM, the previous year’s returns, and the difference between the two.

Takeaways

So, as you can see, the CAPM isn’t really all that accurate when it comes to estimating real-life returns of individual assets, but it was never supposed to be that way in the first place. In the CAPM, every asset is completely diversified, and all unsystematic risk has been eliminated. Furthermore, all assets fall on the SML, or Security Market Line, which has a linear relationship between beta and return. In theory, this is great, but in practice, it doesn’t really fly. The CAPM is still incredibly valuable when teaching students the basics of equity pricing, but it doesn’t have much of a place in our portfolios.