Simulating a Short Strategy

Shorting in Equities Lab

Previously, if you wanted to test out a short strategy, you would have to run your screen and hope that it loses money. That has changed thanks to our new “position_weights” feature where you are able to finally simulate a short strategy more closely and identify if your strategy really does make money.

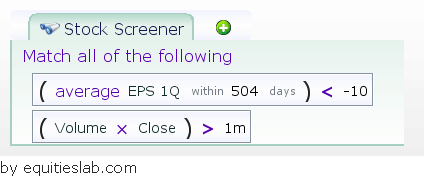

The first thing you need is a strategy. For the purpose of this article, I’m going to quickly throw together a short strategy. Now, this strategy is a total hack, so I wouldn’t use it, but I wanted to include it in order to give you the full story as we continue throughout this article.

Essentially this strategy is just looking for high volume companies that have, on average, lost $10/share every quarter over the past two years. It’s a copout (since that $10 is split adjusted, giving us accidental future predictions), but there aren’t many ways to create a winning short strategy on short notice. Workable short strategies require a little extra effort as you need to check and double check everything since you are dealing with an unlimited amount of liability.

If we run this strategy the way it stands, we will be simulating a scenario where we go long for each position. The idea is that if the strategy loses money it would be good for a short – which is how I’ve gauged these sorts of strategies in the past. However, in the world of shorting stocks, there are a number of variables that aren’t taken account in this model. Variables that we now take into account more thoroughly.

In order to effectively build a short strategy within the Equities Lab system, you need to build two extra tabs.

- Position_weights

- Cash_weight

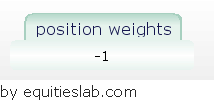

Position Weights

Under the position weights tab, you are going to simply type the number -1. This will give every position in your portfolio a negative weight – shorting the stock. In order to make this strategy realistic, you need to also keep extra cash in your account to lower the risk. This is an extremely important step since there is no cap on how much you can lose when it comes to shorting stocks.

Cash Weight

In this tab, you want to type 2 * number of matches. You need 1 weight to cancel out the share that you shorted and extra cash to cover the losses if the stock jumps enough in price. You multiply this number by the number of matches since you should have about double the cash weight for every stock that you are investing in.

Remember, never think that you can’t lose the money because the stock won’t jump that fast. A stock can triple on good news after close or over the weekend, or really at any point in time that you aren’t able to trade out of the position. Shorting is risky, and it’s better to be safe than sorry. The 2x isn’t required but it’s a good precaution to ensure that you aren’t extended past what your account can handle – landing you in a margin call situation.

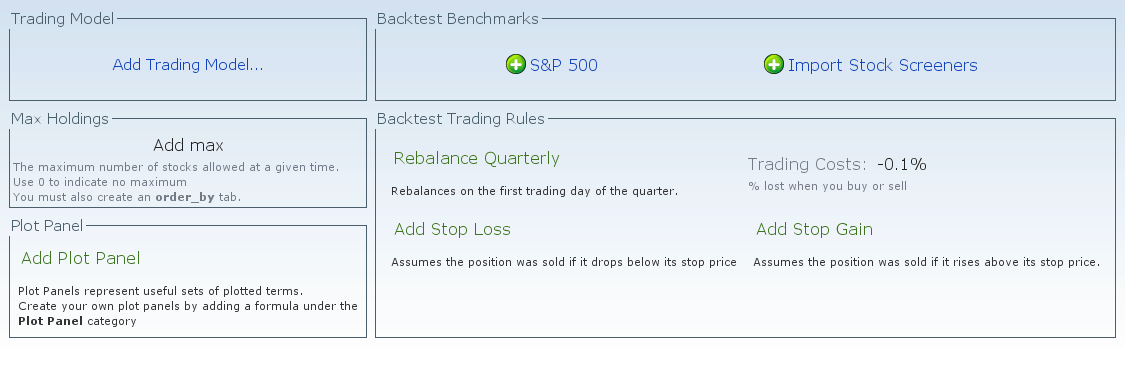

Trading Costs

When it comes to trading costs, you’ll need to calculate them a bit differently when simulating a short strategy. Within the Equities Lab system, trading costs are taken as a percentage of each position’s value. In the case of your short simulation, all of those values will be negative. By adding a traditional trading cost of 0.1% you will actually increase the performance. To accurately reflect the trading costs of your trade you need to add a negative trading cost. Therefore, if your original trading cost was 0.1%, you’ll simply need to adjust that too -0.1%.

How’s the Short Strategy hold up?

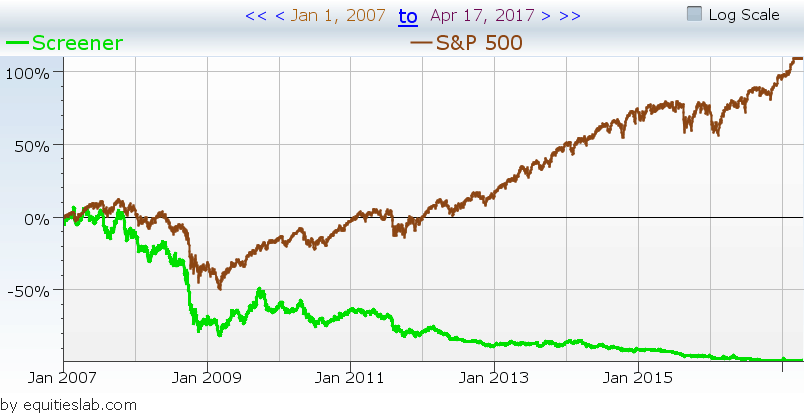

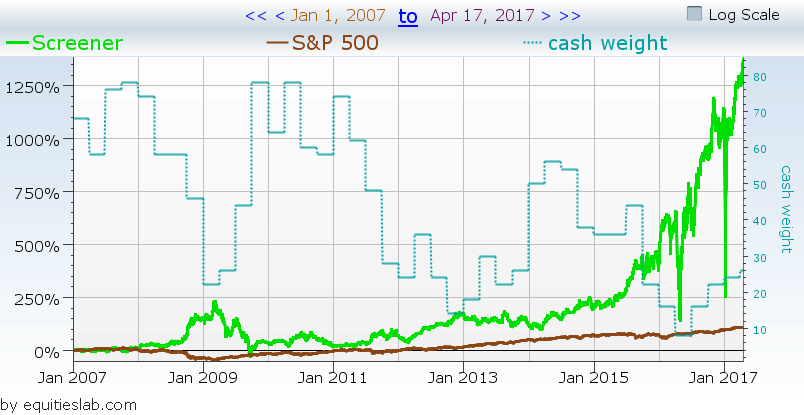

Prior to this added feature, you wouldn’t have had to dive into these extra tabs and trading cost procedures in order to build a “working” short strategy. You and I both would have simply done what we did at the beginning of the article and taken the losses found by going long as gains to be had by going short. Once you actually put these features into place, you’ll find that many short strategies don’t actually do that well over time – especially ones that jumped up significantly at some point. All of that said, let’s see how our little strategy performs over the past ten years after being adjusted.

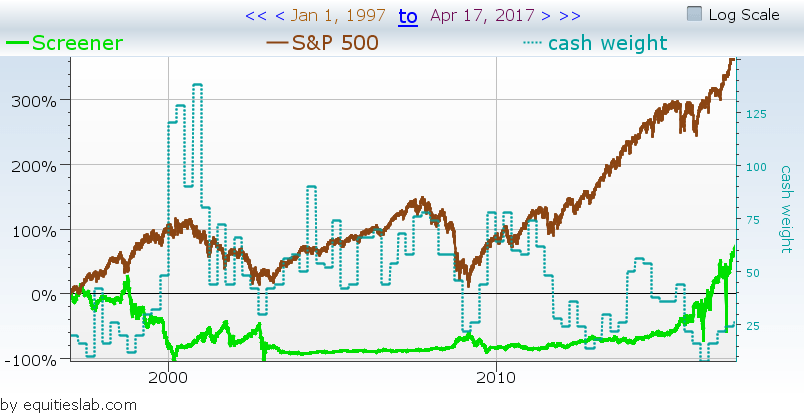

Though the strategy made some money over the past 10 years, there are many times where the account value almost drops to 0 within a very short period of time. Though it didn’t hit 0, it’s indicative of just how volatile and dangerous short strategies could potentially be. Actually, extend the strategy we just put together back to 1997 and you get a strategy that barely makes money over this time period at all, and at one point loses more than 100% of the initial value of the portfolio.