Overview

Crafting Strategies

Backtesting

UI Features

Common Models

Factor Analysis

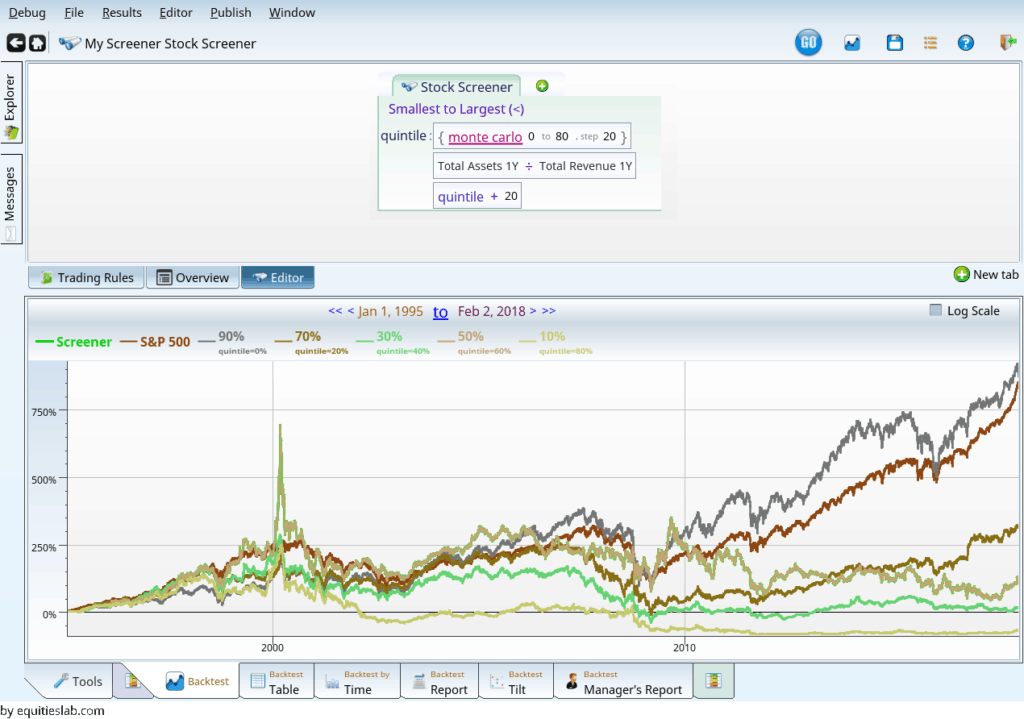

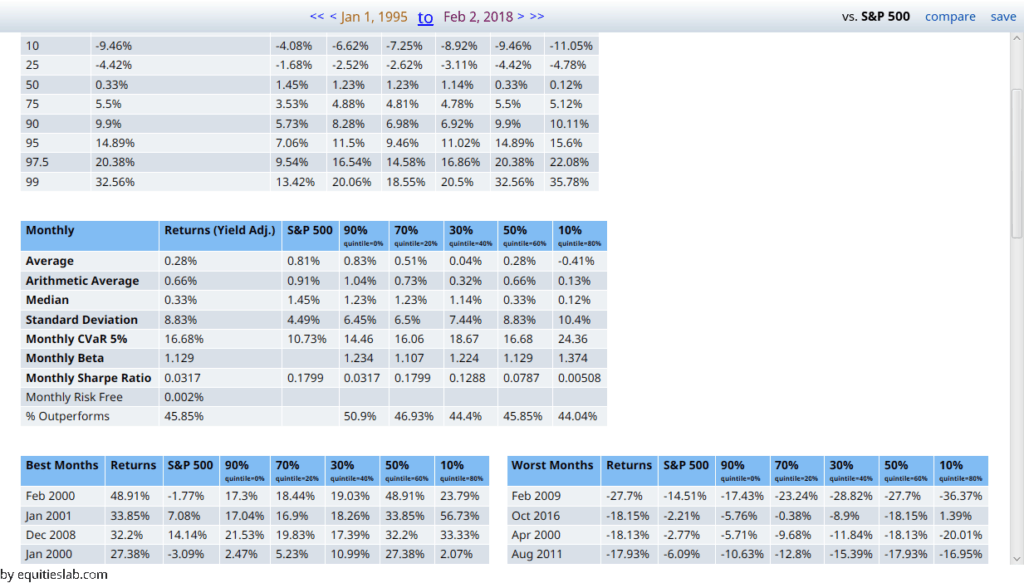

Factor backtesting and analysis

Factor backtesting in Equities Lab is easy, and revealing. Here we analyze the factor total assets / sales, chosen at random because it is late at night when I wrote this article:-).

We see that fewer assets are better: the two best performing quintiles are the lowest ones. If you like numbers better than pretty lines, there are a few below — detailing the performance of each quintile. If you could scroll the scroll bar you could see the yearly performance, but since this is an email, that won’t work…

We have other displays, to dig into the data more, and when you aren’t doing analysis of five backtests at once, you can see the positions taken by each one, so I suspect we can help you out. We use Morningstar data, which goes back to 1995, and we are survivorship bias free, covering US equities.