Overview

Crafting Strategies

Backtesting

UI Features

Common Models

Being too selective with your screener

Guys, you’re being too selective with your screener!

It isn’t uncommon for one of our users to call us up and ask for help. There have even been times when I will help a client at their site to get them up and running, along with follow-up information. In the past two years of working in this industry, I have noticed one major theme among every person (myself included) when it comes to screening for potential investments – we are all far too selective.

What is “Too Selective”?

What do I mean by that?

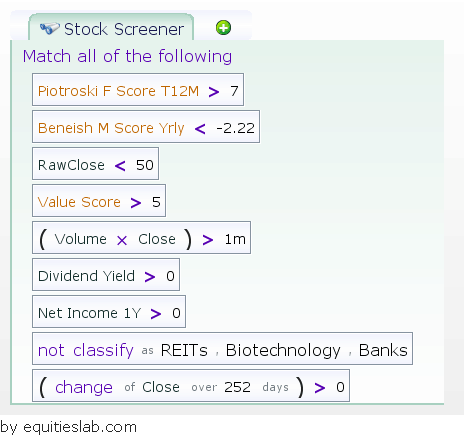

Well, when we go in to start building a screen, we all have the idea of the “perfect” company. This shrunken worldview is just our individual preferences, but it can minimize our potential to make good investments. We go in and build these long screeners that are typically not very complex, eliminating far too many companies from the investable universe and shrinking our opportunities. Screens like this become common –

There are nine total lines in this screener, so the question becomes, how many stocks do you think this screener returns?

The Results

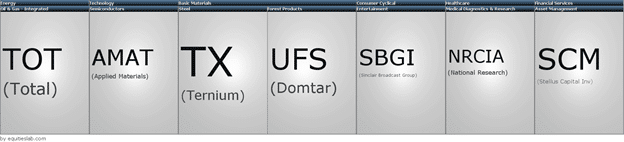

The answer is 7. This screener returns a total of 7 companies. Now, it appears that these businesses are pretty solid. All have everything we are looking for, but with such a small universe, we don’t have anything to compare. If this is what you are basing your portfolio on, you likely aren’t getting any significant diversification. And with only seven choices, you could end up jumping into an investment head first without doing any due diligence.

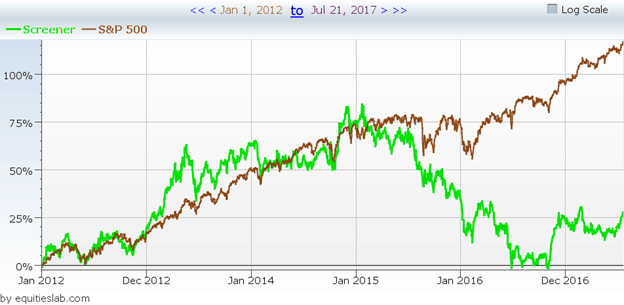

On the flip side, we have built a screen in which most long-term investors would have an interest. They have a high Piotroski score, low Beneish score, affordable closing price, high-Value score, high volume, offer dividends, are making money, increased in price over the past year, and are not in volatile industries. It appears that these companies are solid picks, but how does it perform over the past few years?

In short, horrible. This “perfect” strategy left you hanging, netting you around 25% in the past five years. Even worse yet, you were taken on a complete roller coaster ride with this strategy. You didn’t have any options, and that’s where you went wrong.

What can you do?

The next question you need to ask yourself is whether or not every one of these lines really benefits your screen. How many lines are redundant? How many harm performance and eliminate your potential investment options?

What did we get rid of and why?

- Net Income > 0

- If a company has a high Piotroski score and is financially healthy, it’s pretty safe to assume they are getting some money at the end of the year. By eliminating this line, we didn’t add or get rid of any companies.

- Eliminating certain industries

- Though you may not reflect positively on certain industries, money can be made everywhere. You may have a company pop up that you can’t say no to, and it may very well be a home run. Keep your options open for when you go through and do your due diligence later. Eliminating this line didn’t add any companies, but will keep options open later.

- Dividend Yield > 0

- It’s pretty common to think that companies that offer dividends are inherently better. However, this just isn’t true. Some companies offer dividends they can’t afford and even take on debt to pay them. If we want a dividend parameter, we need to add some extra arguments to ensure the companies are safely offering those distributions. Instead of adding the hassle, let’s eliminate this line and create a dedicated dividends screen later.

- Value Score > 5

- When it comes to building screeners, it is helpful not to use multiple scores –especially if the scores are a “count of” score like the Piotroski and Value score. If you’d like to look at companies based on their scores, I would switch the tear sheet to the score summary and make my own decisions. This issue can also be cured by using the market rank system within the software.

- Change of Close must be positive over the past year

- Though momentum is a thing that works in some cases, it requires a bit of extra effort to get right – much like the dividend screen. It’s also unnecessary in the screener, as we are looking for companies with healthy financials above all else.

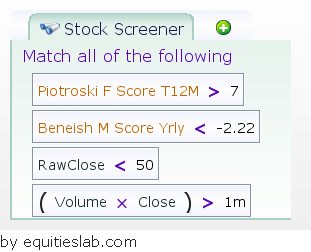

The New Screener

Our nine-line screener has now been cut down to four lines. It’s much more manageable, and we now have room to test different rebalance periods, trading rules, trading costs, etc. Especially since we are now returning 111 companies – giving you way more potential investments.

But, how does it perform?

Going over the past 17 years, we completely crush the market with only 4 lines. I don’t think we will invest in every single company within the 111 companies, but it gives us more options for finding that perfect investment.