Overview

Crafting Strategies

Backtesting

UI Features

Common Models

Backtest Rebalancing

What is rebalancing?

When you first start screening and backtesting for companies you are going to be presented with a number of different variables that need to be decided. One such variable is the rebalance period. Think of a rebalance as the following.

– When a portfolio is rebalanced it is assumed that all positions within that portfolio are sold, and all companies that are returned by the screener are purchased at the same weight at the same time. This activity is portfolio wide and doesn’t include individual position management.

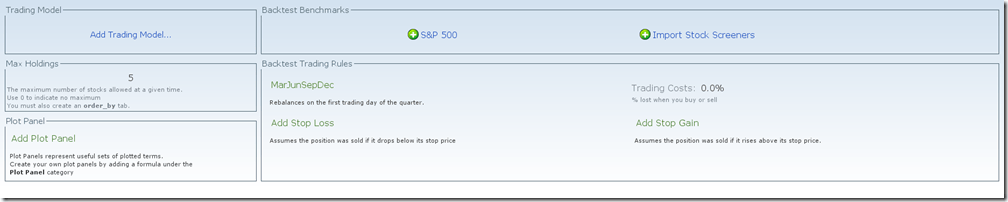

Within the Equities Lab system, you can adjust the rebalance period within the trading rules tab.

The default rebalance period is quarterly, but there are roughly 30 different rebalance periods preprogrammed into the system. If we don’t have the rebalance you’re looking for you can always program your own by creating a new tabbed named “rebalance” and input your parameters there.

The Differences between Rebalance Periods

Since the rebalance period dictates when your strategy trades, you may miss out of some big winners, or buy a company right as it’s about to dive – resulting in different return rates for each rebalance period. The software doesn’t think for itself. You need to be watchful and put in the right amount of time researching each company before you buy it, Equities Lab should only be one stop in your investment process.

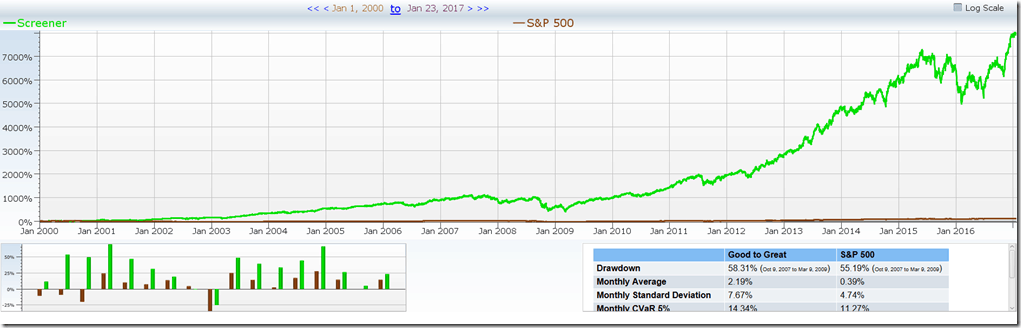

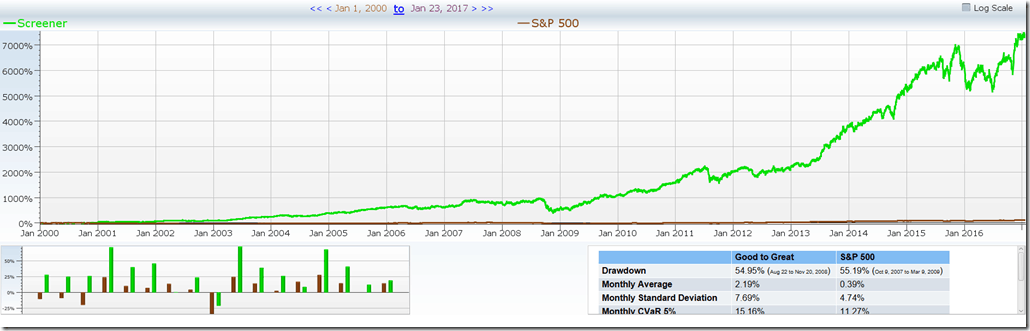

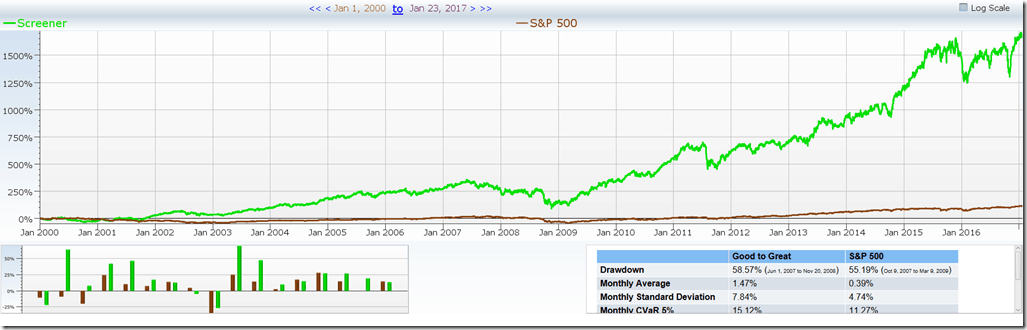

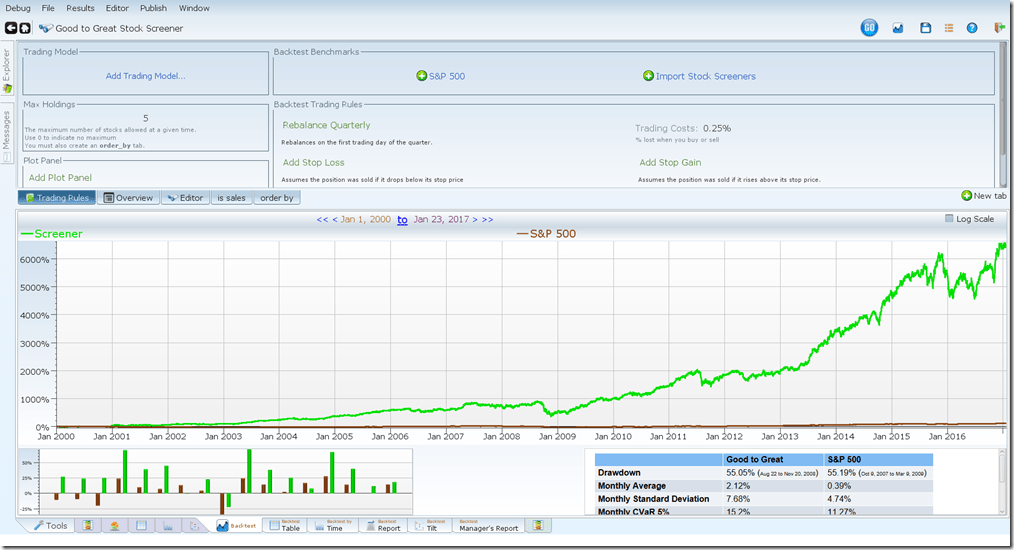

Using our featured screen “Good to Great” I will show you some of the more major rebalance periods – daily, quarterly, and yearly.

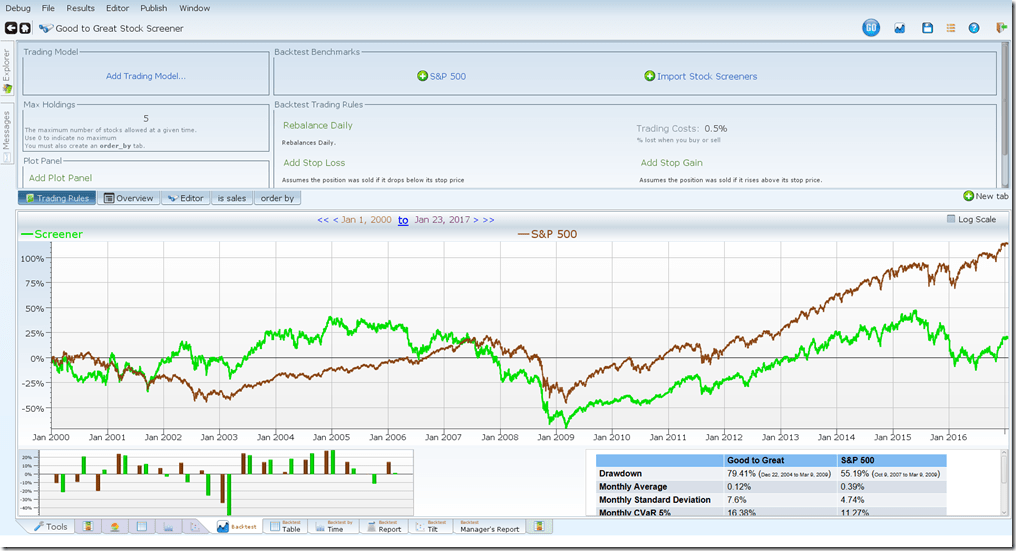

Daily

Quarterly

Yearly

I’m certain you can tell the major differences when you compare the daily and quarterly rebalance periods to the yearly rebalance. There’s actually even a pretty significant difference of almost 1% average per year between the daily and quarterly – making daily more “profitable” than quarterly.

Mind the trading costs

In reality this isn’t necessarily the case. Trading securities isn’t free. It has gotten cheaper as brokers move more of their dealings online and you can get instant executions, but there are still trading costs associated with these investments. This specific screen attempts to cut down on those costs by only returning 5 companies to invest in at any point in time, but the difference between investing on a daily basis rather than a quarterly rebalance is significant.

Since the companies that this screen is returning are fairly high quality investments, we can keep the trading costs down to around .25% for the quarterly rebalance. If you were trading on a screen that found highly volatile investments that you are trading more frequently, you may want to increase that cost to 0.5%+ in order to account for any slippage that may occur.

When you rebalance the screen quarterly, you make a total of 716 trades. Not bad for 17 years of investing. Those trades averaged you 27.83% annually at a 0.2078 Sharpe Ratio.

On the other hand, when we add a trading cost to the daily chart, which performed better than the quarterly chart before, you get a very different result. Here you only make 1.05% annually, making 12594 trades over the same 17 year period, at a Sharpe Ratio of .011.

Stop Losses and Stop Gains

Another way to change up the results of a rebalance is to add a stop loss or stop gain on the trading rules tab or in a custom tab.

– Stop Loss

o A trigger set to sell a position that you have taken on if the underlying stock price drops below a certain level.

– Stop Gain

o A trigger set to sell a position that you have taken on if the underlying stock price increases above a certain level.

These triggers are especially important when looking at screens with a max holdings number set. In the case of the “Good to Great” Screen we only allow 5 companies into it. Say we set a 5 percent stop loss into the strategy; it will sell all positions once they lose 5%. This works wonderfully if you’re trying to cap your losses, but that position is 20% of your current portfolio and won’t be replaced until your next rebalance period. So if you only rebalance once per year, you could very well have exited all of your positions before the next rebalance period, which isn’t something you necessarily want to do. This is just something to think about when setting up your screens and adjusting rebalance period.

In summary

The rebalance feature may not be the most exciting feature within our system, but it is one of the most important. If used correctly it could help you time the market, protect your account from being decimated by brokerage fees, and even improve your long-term returns.